The check processing industry has witnessed considerable growth over the past few years. With the increasing acceptance of digital payments, high risk check processing has evolved and adapted to fit into this new financial landscape. It’s not just about traditional paper checks anymore; these days, electronic check processing, or eCheck, has become a standard practice.

According to a Federal Reserve study, while the overall use of paper checks has declined, the use of electronic checks is on the rise. These industry changes show a shift in consumer preference towards more convenient and fast payment options. As a result, businesses are prompted to adopt eCheck processing to meet customer expectations and remain competitive.

Understanding High-Risk Businesses and Check Processing

Understanding high-risk businesses and their relationship with check processing is a key aspect of the modern-day financial world. High-risk businesses are those considered to have a higher risk of customer chargebacks, fraud, or legal restrictions. These could range from online casinos and adult entertainment sites to travel agencies and telecommunication services.

For high-risk businesses, traditional payment options can be limiting. Banks and other financial institutions often view these businesses as too risky to deal with due to their nature and the industries they function within. As a result, these industries may face difficulty in processing regular check payments and may have to resort to high-risk check processing options instead, which are specifically designed to handle such businesses.

The Challenges in Finding a High-Risk Payment Processor

Finding a high-risk payment processor is often a significant hurdle for high-risk businesses. Since these processors take on the financial risk involved in processing payments for high-risk businesses, not many are willing to do so. Fortunately, companies like EMB specialize in high risk merchants and offer high risk check processing to businesses that need it.

Security is often a critical factor to consider when payment processors evaluate businesses for their services. With high-risk industries being more susceptible to fraud and chargebacks, it is essential to find a processor that offers advanced security measures to safeguard business transactions.

The Issue of Repeat Declines and Limited Options for Payment Processing

Another challenge that high-risk businesses often face is the issue of repeated payment being declined. Due to the risky nature of high-risk businesses, their transactions are more likely to be flagged and declined by financial institutions. This can lead to customer dissatisfaction and potential loss of sales.

Additionally, high-risk businesses often deal with limited payment processing options. Many conventional payment processors are hesitant to take on high-risk clients due to the level of risk involved. As such, these businesses often have to operate with fewer options, which may not always cater to their specific needs.

High Risk eCheck Processing Services

High-risk businesses require robust check processing services to ensure smooth and secure payment transactions. Among the various available methods, eCheck processing services are particularly noteworthy, helping these businesses overcome numerous challenges associated with traditional payment processing mechanisms.

Let’s delve deeper into the intricacies of eCheck processing, its diverse applications, and the emerging trend of high-risk check by phone processing.

Detailed Explanation of eCheck

An eCheck, or electronic check, operates much like a traditional paper check. However, it is processed electronically and eliminates the need for physical handling, thus expediting the entire payment process.

To use an eCheck, the payee needs to enter specific details such as the name of their banking institution, account number, and routing number into a secure online payment form. This information is then used to withdraw funds from the payer’s account electronically, transferring the funds into the payee’s account. This process is entirely digital and typically takes less time than traditional check processing.

Additionally, eChecks follow the guidelines set by the National Automated Clearing House Association (NACHA), ensuring they adhere to secure payment processing standards, thus minimizing the risk of fraud.

The Diverse Uses of eChecks for Various Products and Services

eChecks have garnered much popularity due to their broad application spectrum. Their various uses include:

1. Online Retail: eChecks make it possible for consumers to purchase goods and services online without using credit or debit cards. Therefore, it offers an alternative payment method for those who are hesitant to use credit cards online due to security concerns.

2. B2B Transactions: Businesses can use eChecks to pay suppliers or vendors without the need for a physical check, thus facilitating speedy and seamless transactions.

3. Service Payments: eChecks allow customers to pay for services such as utilities, insurance premiums, and subscriptions, without the need for a physical check or credit card.

4. High-Risk Businesses: eChecks are particularly beneficial for high-risk businesses. They can help reduce the number of declined transactions and improve cash flow by broadening the available payment options.

High Risk Check by Phone Processing: An Emerging Trend

Check by phone processing is an emerging trend among high-risk businesses. It allows businesses to accept check payments from their customers via phone, thereby offering a more convenient and flexible payment method. This service is particularly beneficial for high-risk businesses that might face restrictive limitations with traditional payment methods.

With checks by phone, customers give their bank account information over a secure phone line. This information is then used to create an eCheck, which is then processed electronically. Businesses can later use these eChecks for record-keeping, which helps improve tracking, reconciliation, and potential dispute resolution.

This emerging trend provides another option for businesses looking to add flexibility to their payment processing capabilities. By accepting check by phone payments, businesses are not only catering to customers who prefer this payment method but also improving their operational efficiency.

Remember, implementing high-risk eCheck processing services requires due diligence and adherence to the risk management best practices to minimize potential fraud. As the trend continues to evolve, businesses should continually review their payment processing methods to ensure they remain compliant with regulatory requirements and cater to their customers’ needs effectively.

A Deeper Dive into Common Types of Payment Processing Alternatives

In today’s digital age, businesses must keep up with various types of financial transaction methods to accommodate their customers’ preferences and to ensure the smooth flow of their operations. This section provides a more detailed view of the three common types of payment processing alternatives—eCheck, Check 21, and Automated Clearing House (ACH).

The Distinctive Qualities of eCheck

eCheck, or electronic check, brings the traditional paper check into the digital sphere. It operates by transferring funds electronically from the payer’s checking account to the payee’s account. This transfer happens via the Automated Clearing House (ACH) network, making the process cost-effective and efficient for businesses and consumers alike.

1. How eChecks Work: When customers opt to pay through eCheck, they input their bank account and routing numbers, just like they would write on a traditional check. This data is then carefully processed and encrypted for security purposes, ensuring that the funds are transferred safely.

2. The Advantages of eCheck: Since eChecks essentially digitize the traditional check payment process, they offer several key benefits.

Speed: eChecks process much quicker than traditional checks, which have to be physically transported to the bank.

Security: The use of electronic encryption provides an additional layer of security compared to conventional checks.

Environmentally friendly: As a digital payment method, eChecks reduce the use of paper, helping companies maintain green operations.

Elaborate Step-by-Step Process for Utilizing an eCheck

1. Selecting the eCheck Payment Method: Upon check-out, the customer should select the eCheck option from a list of available payment methods. This redirects them to a secure form to fill out their banking information.

2. Filling the Form: The secure form will request the customer’s routing and account numbers. These numbers are typically found at the bottom of a personal check. The routing number should be nine digits long and the account number can vary in length.

3. Other Information: Depending on the merchant or processor, other information might be required such as the check number, driver’s license number, or social security number to further authenticate the eCheck.

4. Submitting the Form: Once all the required information is filled out, the customer can submit the form. Some processors may send a test transaction to verify the account before allowing the full transaction to go through.

Detailed Procedure for Confirmation of Account and Routing Details

1. Verification of Routing Number: The validity of the routing number is confirmed automatically as it follows a fixed pattern. The routing number identifies the bank that will receive the funds.

2. Verification of Account Number: After the routing number is confirmed, the bank account number needs to be verified. The system checks whether a bank account exists with the provided number and the name of the account holder registered in the bank.

3. Checking Account Funds: The account’s available balance is checked to ensure it can cover the transaction amount. If the funds are insufficient, the transaction will be declined.

Adopting Various Verification Tools to Ensure a Successful Transaction

1. Echeck Verification Services: These services are an efficient fraud prevention measure that cross-checks the check issuer’s history for any fraudulent or bounced checks.

2. ACH Network: Automated Clearing House Network validates the bank account information and checks whether the account is in good standing.

3. Bank Account Validation Tools: These tools are designed to ensure that the provided account details are correct and the account is valid before initiating a transaction.

4. Check 21 Act: Leveraging the Check 21 Act allows for faster processing of the eCheck as it permits the creation and use of a digital image of the original check.

5. Positive Pay: This is a tool used by banks where the account holder provides a list of checks they have issued. The bank only honors checks on that list, thus preventing fraud.

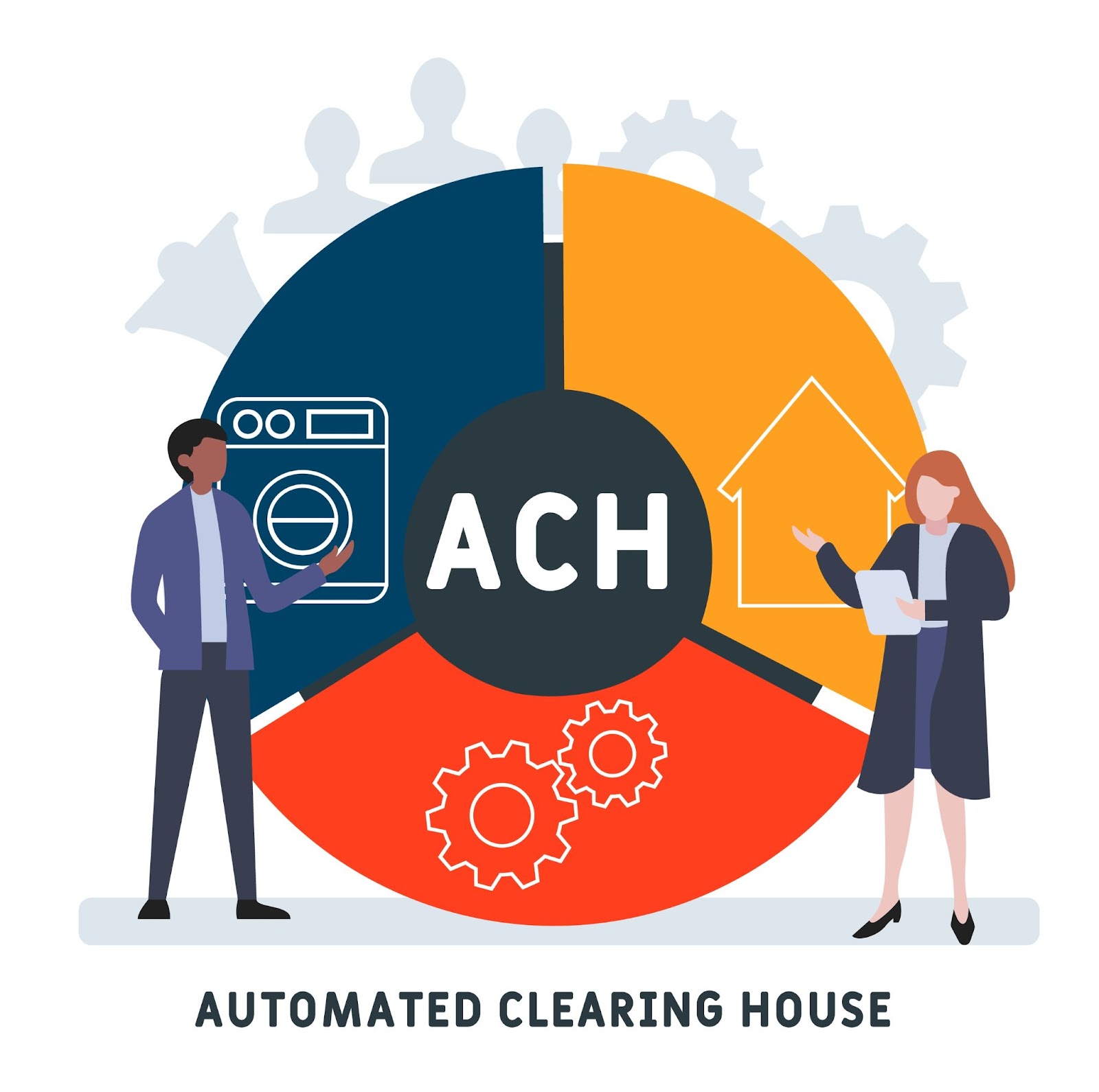

The Surge of High Risk ACH Check Processing in Today’s Market

Before we dive into the in-depth analysis of the Automated Clearing House (ACH) process and its implications for high-risk businesses, it’s vital to have a clear understanding of what ACH entails.

Explanation of ACH Process

The Automated Clearing House (ACH) process refers to an electronic network facilitating a plethora of financial transactions in the United States. Developed and managed by the National Automated Clearing House Association (NACHA), ACH serves as a centralized system that allows financial institutions to efficiently and rapidly transfer funds between bank accounts.

1. The Components of ACH Process

i. Origination: This is where the ACH process begins. It involves a business (known as the originator) initiating a transaction by presenting an ACH file containing transaction data to an Originating Depository Financial Institution (ODFI).

ii. Transmission: The ODFI, upon validating the ACH file, sends it to the ACH Operator (either the Federal Reserve or The Clearing House). This transmission usually takes place in batches, not individual transactions.

iii. Distribution: The ACH Operator sorts the incoming batches and distributes them to the appropriate Receiving Depository Financial Institutions (RDFIs).

iv. Receipt and Posting: The RDFI receives the sorted batch from the ACH Operator and posts the transactions to the recipients’ accounts.

The Emergence and Implications of High-Risk ACH Processing

1. The Ascendance of High-Risk ACH Processing

The rise of high-risk ACH processing can be attributed to the growing awareness and understanding of ACH technology among high-risk businesses, coupled with an increasing need for efficient, cost-effective, and flexible payment solutions. ACH processing can serve as a viable alternative to traditional payment methods, particularly in industries where standard payment options are limited.

2. Implications of High-Risk ACH Processing

The growth of high-risk ACH processing has significant implications for businesses, consumers, and the wider payment industry. Among these we can mention the following:

- Impact on Businesses: High-risk businesses can leverage ACH processing to streamline their operations, reduce costs, and expand their customer base by offering diverse payment options.

- Impact on Consumers: High-risk ACH processing can enhance the consumer experience by offering increased payment flexibility and convenience.

- Impact on the Payment Industry: The rise of high-risk ACH processing signals a broader trend towards the adoption of electronic payment systems and the continuing evolution of the payment industry.

The Advantages of High-Risk ACH Processing

High-risk ACH processing can offer numerous benefits for businesses that encounter difficulties in securing traditional payment processing services due to their industries’ risk profile. Key advantages include:

- Robust Revenue Stream: High-risk ACH processing can help high-risk businesses generate a consistent and reliable revenue stream.

- Lower Transaction Fees: Compared to credit card transactions, ACH processing generally involves significantly lower fees.

- Enhanced Cash Flow Management: ACH payments typically clear faster than traditional checks, improving cash flow management.

- Greater Payment Flexibility: It allows businesses to accept payments in various forms, enhancing customer convenience and satisfaction.

The Limitations of ACH for High-Risk Businesses

While the ACH process, with its low transaction costs and rapid transfer capabilities, can be an attractive option for many businesses, it does have specific limitations that may make it less ideal for high-risk businesses.

- High Return Rates: High-risk merchants often experience high return rates due to insufficient funds, unauthorized transactions, or even fraudulent activities. This not only leads to lost sales but may also result in sanctions imposed by NACHA if return rates exceed the permissible limit.

- Risk of Reversals: ACH transactions can be reversed up to 60 days from the processing date if a customer files a dispute or in case of fraudulent transactions. This exposes high-risk businesses to financial uncertainty and potential loss.

- Longer Settlement Periods: ACH transactions usually take a few days to settle, which may lead to cash flow issues for high-risk businesses that require quick access to funds.

- Stringent Regulations: High-risk businesses often face stricter regulations and may need to comply with additional requirements to use ACH processing. These can include rigorous underwriting processes, demands for higher reserves, and increased scrutiny of transactions.

Storing Customer Payment Information: A Comprehensive Guide

One of the most critical aspects that business owners must navigate in their daily operations involves the secure and efficient storage of customer payment information. Given the progression towards a digital world, safeguarding sensitive payment data has become considerably more significant.

Within the context of high-risk check processing and eCommerce, proper storage of customer payment information can be crucial for the success of a business. Let’s delve into how the storing of this data offers benefits over credit cards and why it requires more information during dispute resolutions.

Advantages of Storing Payment Information Over Credit Card Use

The storing of customer payment information for high-risk check processing, particularly eCheck or Check 21, renders several advantages over traditional credit card data storage. Here are a few key areas where storing payment information outperforms credit card usage:

Reduction of Payment Failures: The use of stored payment information can significantly reduce instances of payment failures. Credit cards can pose problems including expiry, loss, or theft. In comparison, bank account information, which is used for eCheck and Check 21 processing, tends to change less frequently.

Lower Transaction Costs: Processing fees associated with credit card transactions can be higher compared to eCheck or Check 21 processing. Therefore, storing payment information for high-risk check processing can result in significant savings for businesses.

Security: Instances of fraud are rampant in the credit card industry. However, the use of encrypted and tokenized payment data for eChecks reduces the chances of data breaches significantly.

Requirement of More Information for Dispute Resolution

When it comes to the resolution of disputes in high-risk payment processing, it’s crucial to bear in mind that more detailed information may be required compared to traditional payment methods. Here are some key pieces of information that may be necessary:

Account Verification: Before processing the payment, businesses must verify the customer’s bank account details. Verifying these details beforehand can prove useful should a dispute arise in the future.

Transaction History: A comprehensive record of all transactions, including the specific amounts, dates, and items purchased, can be extremely useful in the dispute resolution process. Accurate record-keeping can aid in identifying patterns and resolving disputes faster.

Customer Consent: For successful dispute resolution, businesses should have a record of customer consent for every transaction. This can include digital signatures, emails, or even voice recordings.

Comprehensive Guide to Check 21 System

The Check Clearing for the 21st Century Act (Check 21) was a significant development ushered in by the United States Federal Reserve in October 2004. It was designed to enhance the efficiency of the payment system by reducing the physical movement of paper checks between banks, thus expediting the check collection process.

The cornerstone of Check 21 is the creation of a new negotiable instrument known as a substitute check. A substitute check is a paper reproduction of the original check, containing an image of the front and back, the magnetic ink character recognition (MICR) line, and all endorsements.

Under the Check 21 Act, this substitute check is legally equivalent to the original check and can be used as proof of payment. Financial institutions can present and return substitutes, which means that they no longer need to handle or store physical checks, simplifying the entire processing procedure.

Exploring the Benefits of Check 21 for High-Risk Businesses

In an increasingly digital age, high-risk businesses can leverage multiple benefits from the Check 21 system.

1. Faster check processing: Check 21 facilitates quicker check processing times. Since checks are processed digitally, it greatly decreases the time taken to clear checks, allowing high-risk businesses to access their funds more quickly.

2. Reduction in Check Fraud: Check 21’s substitute checks reduce the possibility of fraud by providing an additional layer of security. Its image replacement documents (IRDs) store digital signatures, preventing check washing and duplication.

3. Decreased costs: High-risk businesses, often constrained by cost, can benefit from Check 21, as it eliminates the need for physical transportation of checks and manual processing. This reduces cost and increases the efficiency of the payment system.

4. Improved Customer Satisfaction: Check 21 enables businesses to offer a more seamless experience to their customers. With faster clearance, customers enjoy quicker access to funds, increasing customer satisfaction and loyalty.

5. Environmentally Friendly: By decreasing the use of paper checks, Check 21 is a more sustainable and eco-friendly solution. This enhanced green initiative can also be a part of the company’s commitment towards a sustainable environment.

6. Enhanced Record Keeping: Digital processing makes record-keeping more efficient and accessible. High-risk businesses can access digital images of checks quickly, making the task of tracking down past transactions more manageable.

The end-to-end electronic image exchange option

A significant benefit of Check 21 is the ability to conduct end-to-end electronic image exchange. This involves the capturing, transmitting, and storing of digital images of checks, allowing for greater ease and efficiency of transaction processing.

Using this method, the check data and images are captured at the point of purchase, converted into an electronic file, and then sent to the bank for clearing. The entire process can be completed within 24 hours, providing businesses with quicker access to funds.

It’s important to note that the success of Check 21 processing relies on its seamless integration with a business’s existing system, ensuring the processing and management of transactions are efficient and secure.

Starting to Accept eCheck Payments

The advent of digital banking technology has significantly changed the way businesses handle payments. This section takes you through the comprehensive process of accepting eCheck payments for your business and shedding light on the benefits for different kinds of merchants. The acceptance of multiple payment methods, including credit cards, debit cards, and eChecks, will also be highlighted.

The Process of Starting to Accept eCheck Payments

Before any business can start accepting eCheck payments, it must first have a merchant account. This account, typically granted by a bank, financial institution or payment processor, allows the business to handle electronic transactions, including those made through eChecks.

Here is the typical step-by-step process:

- Choose a reputable payment processor or financial institution that offers merchant accounts. Your choice should be dependent upon the pricing, customer service, and the processing fees of the institution. Approval rate, ability to scale and choice between multiple gateways should also be considered.

- Complete the application process for a merchant account. This usually includes providing necessary documents, such as proof of business registration and bank account information.

- Once approved, integrate the eCheck processing service with your online store or payment system. This integration can usually be done via an API or through the use of a payment gateway.

- Ensure that your website complies with all necessary security standards. In particular, it should have an SSL certificate to encrypt all transaction data.

- Finally, test the eCheck processing service to ensure that it works correctly before accepting payments from customers.

Benefits for Recurring Billing and Large Ticket Merchants

eChecks offer distinct benefits for businesses that operate on a recurring billing model or for those that handle large ticket transactions. Here’s why:

Recurring Billing Businesses: eChecks are ideal for businesses that rely on subscription-based models or have routine billing cycles. This is because once a customer authorizes an eCheck transaction, the merchant can reuse the same banking information for future transactions, ensuring seamless payments.

Large Ticket Merchants: For businesses that sell high-cost items or services, eChecks can be a cost-saving solution. This is because eCheck processing fees are often lower than credit card processing fees, especially for large transactions. They also offer a higher level of transaction security, minimizing the risk of chargebacks.

Acceptance of credit cards, debit cards, and eCheck payments

Accepting multiple forms of payment, including credit cards, debit cards, and eChecks, can be advantageous for businesses. This gives customers more flexibility and payment choices, which can subsequently lead to increased sales and customer satisfaction.

The infrastructure for accepting these payment methods can be set up simultaneously when establishing the merchant account, making it an efficient business decision. Hence, offering those options, in addition to eCheck payments, ensures you cater to a broader customer base.

Overall, the process of starting to accept eCheck payments involves choosing a merchant account provider (like EMB), integrating eCheck processing into your existing payment systems, and complying with all necessary security standards. By offering eCheck payments, businesses can benefit from fewer disputes, advantageous conditions for recurring billing and large ticket merchants, and a widened scope of payment options for customers.