- About Us

-

Solutions

The Payment Experts

Our integrations connect you with the best tools for your business.

Integrations - Partner

- Industries

- Contact Us

Start accepting eChecks today

Electronic Check Processing

Opening up your business to accept as many forms of payment as possible opens you up to more transactions — which means higher top line revenue. You do not want to turn your customers down, so open the door to more customers and increase sales revenue.

Electronic check processing, also known as eCheck processing, is a valuable service that allows your business to expand payment options. By accepting eChecks, your business can provide customers with a safer and convenient payment method while reducing the risk of chargebacks and fraudulent activity.

High risk check processing with eCheck:

Checks by web

Our checks by web service lets customers purchase goods and services from you without a debit or credit card. It provides a safer payment option, and cuts back on chargebacks and fraud.

Checks by phone

Our checks by phone service allows merchants to accept and process checks over the phone. It comes with five basic features and a variety of benefits to make processing checks simple.

Paper guarantee

This service removes the risk of check payments with a 5 step process to instantly prevent fraud and protect you if a check bounces.

- Best Merchant Services: Top Providers for Your Business NeedsThe success of your ecommerce business depends on conversion. A large part of creating these… Read More »Best Merchant Services: Top Providers for Your Business Needs

Open the door to more with eCheck processing

Why bother with check processing? Merchants are charged smaller fees to process e-checks than credit card payments. E-check processing is a popular choice for high-ticket items like jewelry and electronics, and services like fitness memberships. Think of it as another weapon in your arsenal as a business — another way for you to service your customers.

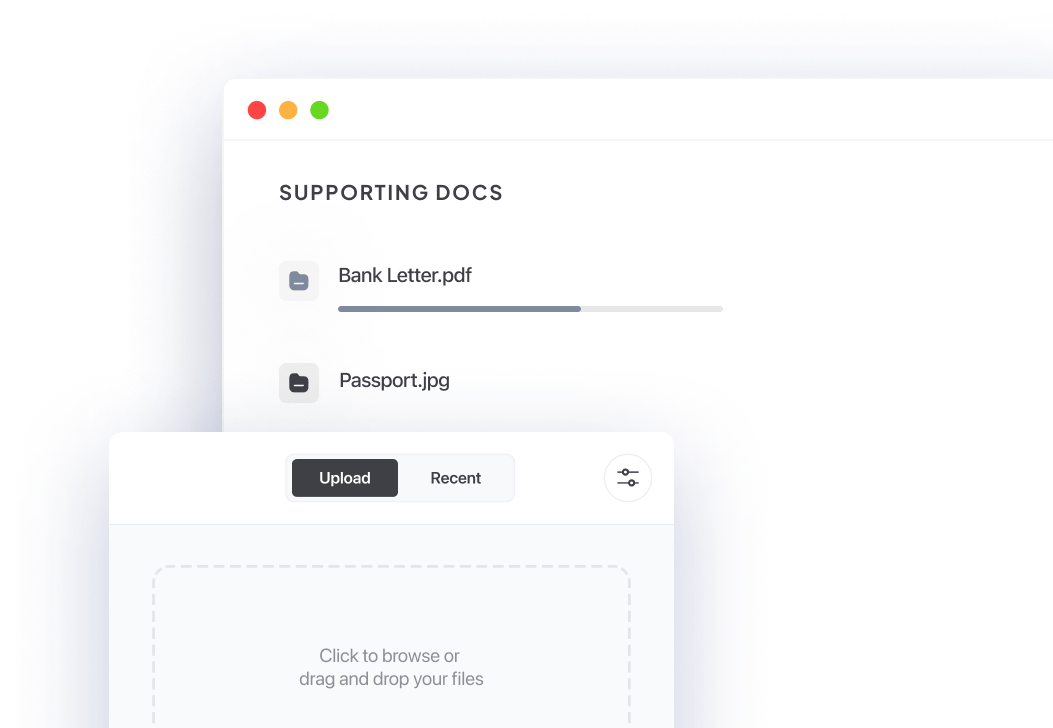

What documents are required?

We make the online application process simple. While we can’t promise guaranteed approvals every time, we can promise a fair process. In addition to a completed application, you must provide the following documents:

- Copy of passport or ID

- Corporate documents

- One month of business bank statements (if available)

- Bank letter or confirmation of deposit bank info showing business name, IBAN or Swift information

Streamline your payments with electronic check processing

If you’re looking for a way to streamline your payments and improve your cash flow, consider signing up for electronic check processing today!

Don’t just take our word for it

“Marlin knew many of his business’s clients felt safer using paper checks. But he found looking for a quality eCheck processor a daunting task. With EMB’s eCheck processing service, eCheck Plus, we were able to offer Marlin and his business the ability to process checks electronically without having to purchase or install additional software or hardware, and see the funds from check sales right away.”

Marlin T. Roche, small business owner

“Sanj Kumar’s ecommerce business experienced an influx of fraudulent chargebacks from international customers due to the nature of its luxury business. Experiencing regular instances of fraud was having an impact on profit margins and the future of its merchant account. Based on EMB’s knowledge of the industry and broader fraud trends, we were able to offer Sanj timely and effective policy changes to his fraud protection program. ”

Sanj Kumar luxury ecommerce business owner

By using electronic check processing services, your business can accept check payments instantly, making it easier for customers to purchase goods and services from you without a debit or credit card.

Check processing services allow businesses to accept and process checks through various methods, such as checks by web, checks by phone, and paper guarantee, making it a safer and more convenient payment option for both customers and merchants.

Electronic check processing services enable businesses to accept and process check payments electronically, reducing the risk of fraud and chargebacks, and streamlining the payment process for improved cash flow.

Yes, you can accept checks online using echeck payment processing services, which let customers purchase goods and services without a debit or credit card, providing a safer payment option and cutting back on chargebacks and fraud.

Echeck payment processing is a method of processing check payments electronically, allowing businesses to accept checks online or over the phone, providing convenience and security for both customers and merchants.

Echeck payment processing time can vary depending on the provider and specific transaction. However, it is generally faster than traditional check processing, with funds being available within a few business days.

Echeck processing involves electronically capturing the check information, submitting it for processing, and depositing the funds into your business account, streamlining the payment process and improving your cash flow.

When customers choose to pay with an echeck, they provide their bank account information, which is then processed electronically, allowing for a faster, safer, and more convenient payment method than traditional paper checks.

Check payment processing offers businesses the ability to accept checks online or over the phone, providing customers with a convenient and secure payment option, reducing the risk of fraud and chargebacks, and streamlining the payment process for improved cash flow.

Still have questions?

If you can’t find the answer you’re looking for, please reach out and chat with our team.

Get in touch